India’s July 2020 headline CPI (Consumer Price Index) grew 6.9% year-on-year (y/y), above expectations, on the back of an upward-revised 6.2% for June. Although the food component was slightly higher than expected, it is the higher core CPI (ex food & beverages, fuel and light) which was really surprising. However, the details warrant careful assessment before making any conclusions on the strength of this reading, its drivers and the path ahead for inflation.

The broad macroeconomic backdrop remains one of contractionary growth and the drop in demand it entails. The imputation methodology followed in April and May to construct some of the CPI components, when price collection was limited, added to the data-noise and assessment-issues. It should ideally auto-correct from June as real prices become available for more components as well as from higher number of markets for each component. However, the revisions for June, the readings for July and its split into rural and urban raises more questions for now, than answers.

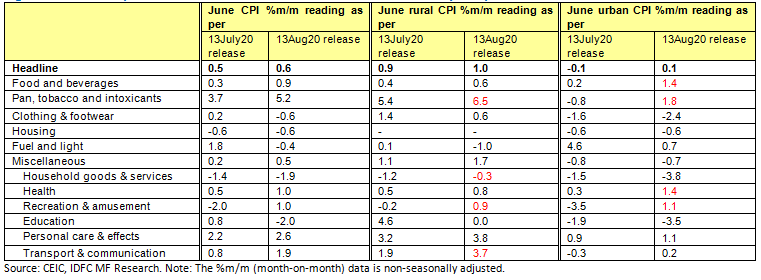

Figure 1: June CPI upward revision - minor headline revision masks heavy component revisions

Observations:

1. Firstly, the June CPI headline number was revised higher from 6.09% y/y to 6.23%. Although the headline revision was marginal, some of the sub-indices underwent major revisions. They offset each other for a net impact of only 14bps. This makes the starting point of assessment of the underlying inflation drivers more unclear.

2. The June core print was mainly driven by rural, which had previously made us look at the possibility of stronger rural demand, albeit difficult to sustain, as supply-side constraints also applies less to rural vs. urban. The revised numbers point to an even-stronger rural core momentum in June. However, what stands out among the major drivers of this are that inflation in a) household goods & services (washing soap, domestic servant, etc.) were revised higher in rural but much lower in urban, b) recreation & amusement was revised much higher in both rural and urban (the magnitude is surprising although the category includes cable TV charges which could have gone up) and c) transport & communication was revised much higher for rural vs. urban (despite the major components expected to impact them similarly).

3. The reason for the sharp downward revision in fuel & light, particularly in urban, is not clear and does not correlate well with the revival in demand for electricity and the price of LPG (Liquefied Petroleum Gas) in June which is also typically available well on time.

4. The higher urban food & beverages inflation could be mainly attributed to the higher demand for essentials vs. discretionary although detailed data suggests while prices of cereals, pulses, vegetables, fruits, meat and fish have been revised higher, that of milk, sugar and prepared meals have been revised lower for both rural and urban. Higher pan, tobacco & intoxicant prices should be due to the higher taxes

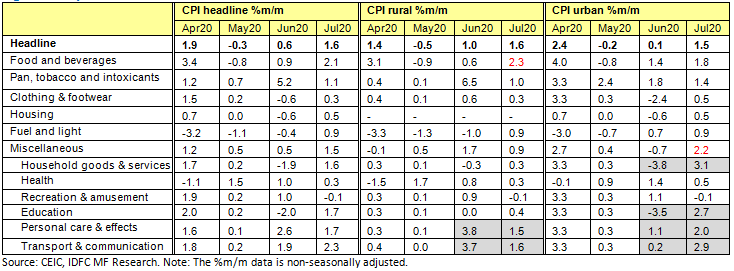

Figure 2: July CPI - driver of core CPI shifts to urban while that of food shifts to rural

5. In the latest July print, we see food inflation picked up very strongly in rural India driven majorly by vegetables. This raises the question whether it is actually supply-side issues for perishables which have been driving up their prices in urban India.

6. Momentum in fuel & light also reversed sharply for rural alone, although this seems to be due to higher prices of public-distribution-system-based kerosene and coke.

7. The more intriguing aspect in July is the sudden change of the driver of core CPI from rural to urban. Prices of urban household goods & services and education picked up sharply, while rural momentum in these stayed soft, despite moving higher from June. The reasons for this sudden reversal in urban prices is again unclear.

8. Further, the momentum in personal care & effects (includes gold) and transport & communication (petrol mobile charges, bus fare, etc.) picked up sharply again for urban CPI, while it eased for rural.

Summary:

The macroeconomic narrative is of contractionary growth and a drop in consumption demand from households because of falling income, rising precautionary savings and even inability to spend due to local lockdowns to combat the spread of the virus. However, after the April and May CPI data was only provided for the sake of continuity using imputation methodology as price data collection was limited, CPI readings from June onwards were expected to be based on more actual data and thus improve assessment. However, the upward surprise in the July CPI, particularly for core, is difficult to ascertain at this point (owing to the observations made above) and seems more difficult to be purely attributed to a pickup in demand and/or supply constraints. This warrants ongoing careful assessment of data before making conclusions about the surprising strength of the CPI, its driver (rural vs. urban) and its likely path ahead.

On monetary policy, given the RBI mentioned last week it will look for a ‘durable reduction in inflation’, this reading could potentially reduce the probability of an October rate cut as the Monetary Policy Committee (MPC) will have only July and August CPI readings for its meeting on 1st October. However, the bigger picture now is the diminishing utility of incremental rate cuts and the case for lower-for-longer policy rates.

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the stocks may or may not continue to form part of the scheme’s portfolio in future. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.