The bond market had been understandably perturbed in the run up to the October policy. The so called Variable Rate Reverse Repo (VRRR) cut off for a shorter tenor had spiked at quarter end thereby muddling some expectations with respect to the normalization plan ahead. The global backdrop has been turning more hostile as well with a more hawkish Fed leading US real yields (and dollar index) higher and with energy prices skyrocketing. Clouding formation of expectations has also been the fact that the level of the overnight rate indeed is still at emergency levels in India. This has looked all the more discordant given the resurgence in organized sector recovery that one has seen over the past few months.

RBI’s policy description today hence comes as a welcome reorientation for market focus. It reemphasizes the importance given to continuity and nuanced interpretation that one has seen over time in the current regime. That said, it covers substantial further ground in the path towards policy normalization but continues to respect for the most part the importance of market signaling (and thereby the risk of signal amplification if market isn’t guided well). Thus all rates were kept unchanged but more importantly the guidance with respect to the accommodative stance was retained: “as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward”. The dissent on stance by one external member was carried forward from the last time.

RBI Assessment and Measures

While real GDP growth for the first quarter of this financial year printed somewhat shy of its assessments, RBI / MPC remain upbeat about how the recovery has progressed post the 2nd wave. Apart from the ever-present risk of new virus waves, most of the risks to growth are actually external in nature as per the central bank’s assessment. Growth is slowing in some major Asian and advanced economies, there has been a steep jump in natural gas prices recently, and there are concerns emanating from normalization of monetary policy in some major advanced economies. Thus RBI / MPC conclude that “against this backdrop, the ongoing domestic recovery needs to be nurtured assiduously through all policy channels”. Adding fuel to this is the observation that even as the outlook for aggregate demand is progressively improving, output is still below pre-COVID level and the recovery is uneven and critically dependent upon policy support. Compared to pre-pandemic levels, contact intensive services, which contribute around two-fifth of economic activity in India, still lag considerably. Capacity utilization in the manufacturing sector is below its pre-pandemic levels and an early recovery to its long-run average is critical for a sustained rebound in investment demand. Hence, even with a dramatic improvement there is considerable room to cover.

On inflation, core and fuel pressures persist but owing to softening in food prices July – August readings were lower than expected. Importantly, the outlook on food inflation continues to be benign given the recent catch-up in kharif sowing and likely record production, along with adequate buffer stocks and relatively contained recent volatility in vegetable prices. However, the recent resurgence in edible oil prices is flagged as a concern. Also rising cost pressures are a concern though weaker demand is mitigating pass through into product prices. There is again an appeal to the government to cut tax on fuels. All told, however, the expected inflation trajectory is now lower thereby providing that additional comfort to monetary policy for the time being.

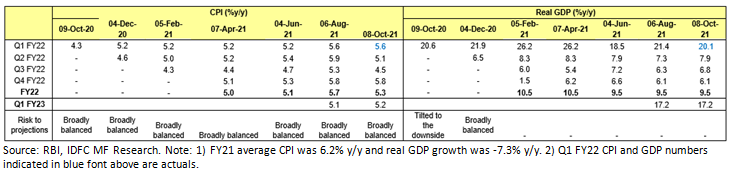

The table below summarizes changes to forecasts:

On liquidity RBI recognizes the heavy surplus in the system and has taken 2 important steps (one of which was fully discounted and the other broadly expected by many in the market):

- The 14 day VRRR quantum is being further hiked from the current INR 4 lakh crores to INR 6 lakh crores in stages by December. Further, depending upon evolving liquidity conditions, RBI is also open to introducing 28 day VRRR in a similar calibrated fashion. However, there is clear communication that this is basis market feedback, and a reiteration that enhanced VRRRs should not be interpreted as a reversal of the accommodative policy stance.

- RBI is discontinuing the so-called GSAP or the assured government bond buying program, even as the usual commitments to orderly evolution of the curve and availability of all instruments as needed remains. This is reasonable and consistent with the view on liquidity and a relatively more hands-off evolving approach to the bond market. Nevertheless, here RBI can show its hand from time to time depending upon its qualitative views on orderly evolution.

Analysis and Takeaways

We have recently explained in detail our current bond framework (https://idfcmf.com/article/5730). We do believe that the current level of overnight rate is at emergency levels and has to be lifted soon enough. That said, a view on when to lift this is a matter of perspective and RBI’s threshold on the amount of assurance it wants on growth being self-sustaining is probably somewhat higher than what many in the market (including ourselves) may have. However, we don’t believe that just basis this one can characterize RBI as being behind the curve. This follows from the other pillar of our framework, which arguably is more important at this juncture now that the process of normalization is underway: peak policy rates in this cycle are likely to be lower than in the last. Therefore even if RBI’s view is towards a later lift-off, given our expectation of a shallower normalization cycle anyway, we would be loath to characterize it as being behind the curve.

We provide some macro data below to buffer our point.

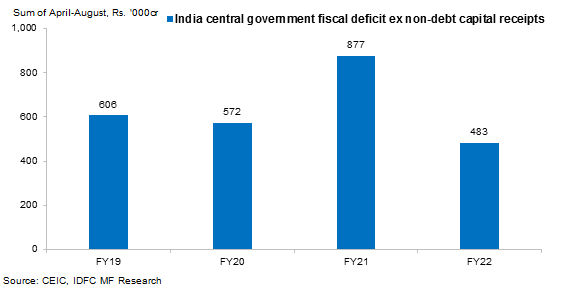

The figure above tracks absolute central government deficit (in INR crores) year to date this year with similar periods in the last 3 years. We have adjusted the deficit for capital receipts in order to arrive at ‘true’ deficit. As can be seen the actual deficit in value terms (not as percentage of a volatile denominator) between April – August this year is lowest in the last 4 years. Thus even from a relatively nuanced fiscal response last year, the government has moved to rapidly consolidate its deficit (at least so far). This allows for monetary policy to remain ultra supportive for that much longer, ceteris paribus.

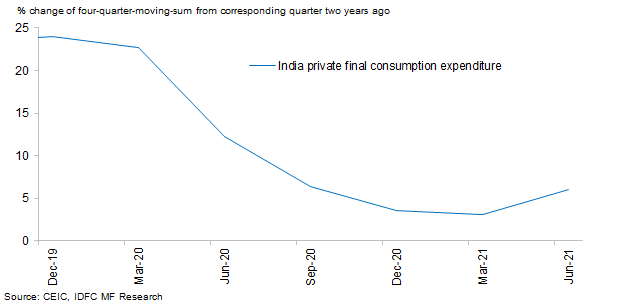

The next chart tracks India’s private final consumption expenditure (PFCE) growth. In order to smoothen the volatility owing to Covid, the graph above tracks percentage growth in 4 quarter moving sum of PFCE versus the same 2 years ago. As can be seen this had fallen off very sharply and, while recovering, is only doing so quite slowly. Thus while recent evidence does point to a strong rebound, longer term data shows a still slow return to a robust growth in aggregate spending and even then no where close to the heady times of a few years back.

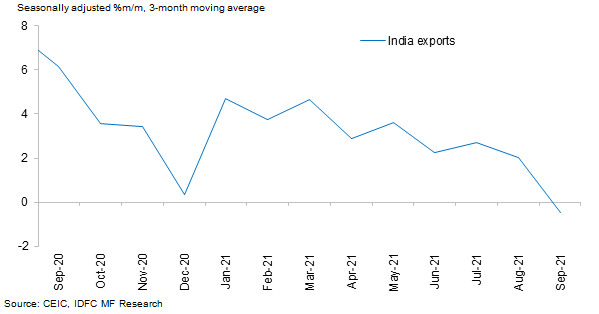

The chart above tracks recent momentum (month on month growth seasonally adjusted smoothened by considering 3 month moving averages) in India’s exports. Recall that exports have been a notable engine of our growth over the past few quarters. As the chart shows, the momentum has been distinctly slowing over the past few months. While this is relatively short term data and momentum can always pick up again (especially given all the government measures around manufacturing for exports) we still can’t help but notice that our export momentum peaked right about when global growth generally peaked. With a clear possibility of more volatile global growth from here on (a point noted by RBI / MPC as well), this is something that would merit close attention. Also from an aggregate demand identity standpoint, the above two charts clearly support the patient stance from RBI given that that they represent two important pillars of demand.

In all then, while near experience is definitely of resurging demand, there is still enough justification for patience from RBI / MPC especially when looked along with the evolution of fiscal deficit so far. This is truer if one remembers that monetary steps impact economic activity with considerable lags. Therefore, the importance of securing a clear runway for growth becomes all the more understandable. On the other important issue of addressing savers’ needs, as the Governor highlighted in the press conference, the government is part mitigating the issue by keeping small savings rate much higher and thereby subsidizing investors accessing those instruments to that extent. As a general point, and one we have made before, while both are important parts of the system the relative importance of consumer versus saver keeps shifting depending upon which point we are in the macro / growth cycle.

A Word On Portfolio Strategy

Our bond framework note had discussed our current portfolio strategies in detail. Our one slight disagreement with market consensus is probably with respect to what we think is the best play for the policy normalization cycle that has already commenced in some way. Thus in our view 5 – 10 – 15 year spreads are unlikely to narrow much from here (bulk of flattening will happen between 1 and 5 years and various combinations therein, of course this is as per market consensus view as well) whereas at least recent price action seems to suggest that general market opinion is that 10 and 15 year points provide better safety. We say this because despite a much lower borrowing calendar for the second half of the year in the 5 year space, we didn’t see an appreciable tightening of spread between 5 and 10 years (of course ‘technical’ factors could be at play as well, including that we are being too impatient with this!). Our view is basis our third framework pillar that bond demand versus supply dynamics may remain a longer term issue. The discontinuation of GSAP is (at least temporarily) leading to some steepening between 5 year and longer but our issue is much longer term.

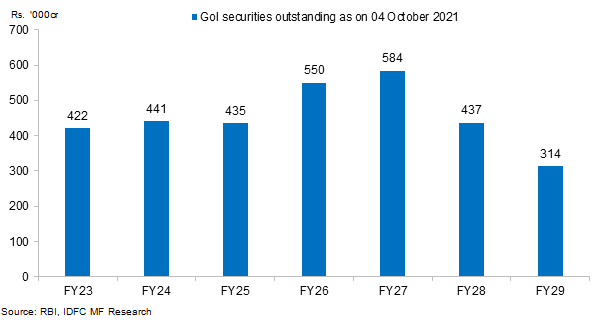

As can be seen from the graph above, there are very large government bond maturities lined up for the next 5 – 6 years. This means that gross bond supply will likely be large during this time even with gentle fiscal consolidation. Furthermore, bond switching operations that RBI undertakes on behalf of the government will also have to focus on reducing outstanding in this bucket. This implies that focus of net bond supply will necessarily have to be for longer durations, which combined with a start point of a not particularly steep 5 – 10 – 15 years makes the 5 year point quite attractive, relatively speaking. Finally, the 5 year has roll down benefits (the current bond is already 4.5 years) which isn’t apparent immediately in the 10 and 15 year segments. Thus even if the 5 – 10 – 15 year spread doesn’t compress, the roll down of the 5 year over time will automatically ensure greater steepness to longer duration points. Given this, we continue to be heavily overweight 5 year (4.5 years now) in our actively managed bond and gilt funds. As before, and as a matter of standard disclaimer, what has been presented here reflects our current thinking. As always this can change at any point in time.

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.