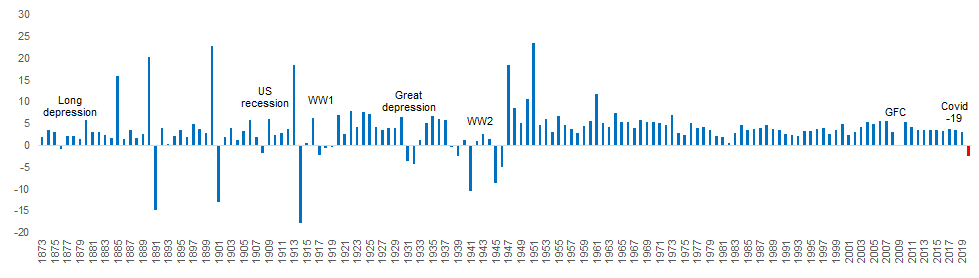

As the COVID-19 outbreak evolved into a full-blown global pandemic, various countries, including India have introduced lockdown measures. This has crippled economic activity, repressed trade & substantially driven up unemployment. The economic consequences of the pandemic are impacting all countries with unprecedented speed and severity. As can be seen from the chart below, the global Gross Domestic Product (GDP) growth is likely to experience its largest fall since World War 2. In a three-week span ending Apr 4, nearly 17 million Americans have now applied for jobless claims (nearly ten times the pre-COVID-19 high), which translates to about 10% in terms of the unemployment rate while the euro area final Purchasing Managers Index (PMI) composite output index has fallen by 21.9 points in a month to a new all-time historical low of 29.7.

Global GDP

Source: Maddison Project Database 2018, IMF, IDFC MF Research, COVID- 19 forecast is average of estimates of private forecasters

The current economic crisis resulting from the COVID-19 pandemic is in many ways worse than the 2008-09 recession which was primarily a financial crisis originating from the US housing & banking sector. It could be addressed by easing the financial conditions before it contaminated the mainstream economic activity. The COVID led contraction on the other hand, could result in cascading of bankruptcies, defaults, unemployment, and consumer scarring could have a deep & lasting impact on global economy. Getting ‘back to work’ could take time, and more importantly getting ‘back to leisure’ i.e. discretionary consumer spending could even take longer.

Explicably, the central banks & parliaments are throwing their whole might behind the system to contain long lasting damages of COVID to their economy.

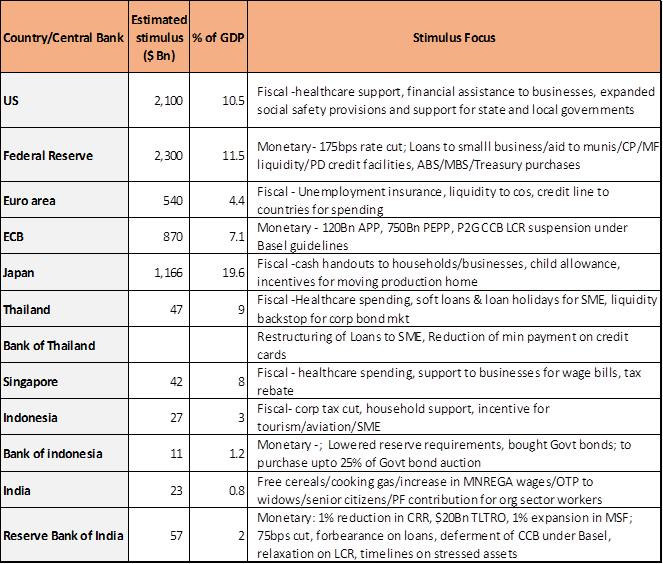

US congress has already approved a massive $2.2 trillion fiscal stimulus (10% of GDP) dwarfing even its post world-war 2 (6.6% of GDP) & 2009 stimulus efforts (8.7% of GDP) with another $1 trillion stimulus under discussion. Meanwhile, Federal reserve cut rates to record low, pledged to buy unlimited amount of US treasuries (purchased over $1 trillion securities since the announcement), & is providing incremental $2.3 trillion in credit/liquidity to the mainstream economy through its various facilities.

Below is the snapshot of different stimulus responses by various countries (representative and non-exhaustive):

Source: Respective Government , central bank announcements, CP- Commercial Paper, MF- Mutual Fund, Munis- Municipal bonds.ABS/MBS Asset Backed Security, Mortgage Backed Security. P2G: Pillar 2 guidance, CCB: Capital conservation buffer, LCR: Liquidity coverage ratio, APP: Asset Purchase program, PEPP: Pandemic emergency exchange program

Impact of COVID-19 on India

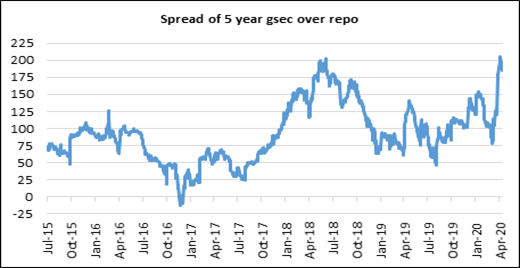

Even before COVID-19 hit India, policymakers were grappling with multiple challenges to growth. The Indian growth story has been mainly held by 2 pillars in the last 5 years i.e. private consumption & Govt. spending. The household consumption driven by leverage rather than job/income growth had started to decline as shadow banks pulled back after asset quality concerns in their loan books. The real estate & SME heavy banks/NBFCs continued to be shunned by asset markets with their looming failure threatening macro stability. The 2nd pillar- Govt. spending was also under constraints. The financing of fiscal deficit was increasingly coming in question with huge reliance on nontax revenue & off-balance sheet expenditure. Real bond yields were becoming untenable due to heavy supply in a period of risk aversion in the banking system.

As can be seen in the chart, Govt bond/repo spreads remained extremely wide & rate cut transmission remained weak despite record surplus liquidity/low credit growth & recurrent bond buybacks/yield curve management (Operation twist) by RBI.

Source: Bloomberg; Data till 15th April 2020

The onset of COVID has hit India in multiple ways. The spillover of global GDP contraction, industrial shutdowns & disruption in supply chains could be significantly severe for India with 50% of labour force in self & 25% in casual employment - primarily outside any safety net. Another channel of disruption would be the fall in private remittances to India from Gulf & US. There is also an increased possibility of second order impact on financial/real estate markets which could further erode household’s wealth in an environment of job losses, accelerate defaults & further impair already weak NBFC/bank’s balance sheets.

Most of the private forecasters & multilateral agencies have downgraded India’s growth estimates & pegged our growth rate between 1.5-2.8% provided the domestic contagion is contained. The growth impact could even be more severe as the lockdown is getting extended. Understandably there are demands across industry for further support from Govt and RBI. In fact, NAREDCO & ASSOCHAM have asked the govt. for a $200 - $ 300 billion stimulus (10% of GDP) in next 12 months.

Given the economic, social & human costs, while there is a need of a meaningful stimulus & probably India wouldn’t be seen as indisciplined outlier, it is worth examining if we have the artillery before we ask for the “bazooka”.

High fiscal deficit - Space for Stimulus?

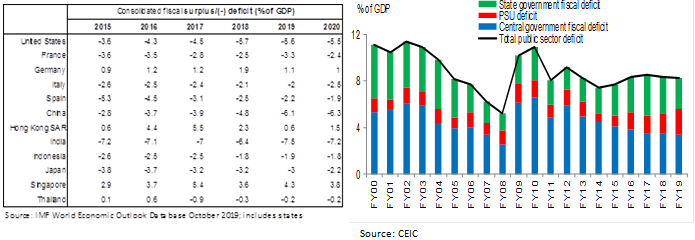

While there is near unanimity in need for countercyclical measures, there is also a concern whether India has meaningful headroom available unlike the US which enjoys the “exorbitant privilege” of dollar or even ECB or BOJ which are considered the tier 2 reserve currencies. As can be seen below, prima facie India does appear to be in a quandary unlike some of other economies

In fact, if we consider the rising PSU borrowings, the real deficit pre-Corona is close to FY09 high. In fact, the Govt. was being criticized for high fiscal deficit & crowding out private sector investment pre-Corona.

Is Govt. crowding out private sector?

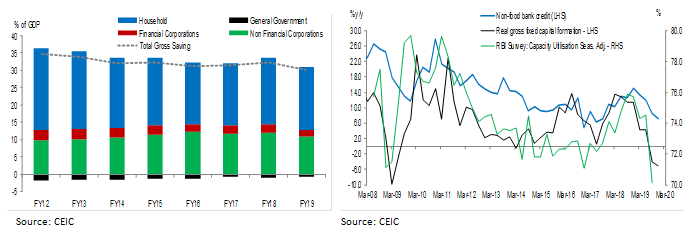

While there is a concern that a sustained high fiscal can starve funds for private sector, a closer analysis of their capital expenditure, credit demand & capacity utilization suggests otherwise. As can be seen from the chart below, it’s the low consumer demand as evidenced in low capacity utilization/low capex which is possibly leading to low credit growth & not just higher borrowing costs. Given that consumer demand is likely to remain muted in the medium term & private sector capex is unlikely to pick up soon, Govt. can definitely step up its borrowing without diluting private credit demand. As can be seen in India’s Gross Saving (% of GDP) chart below, private sector saving has remained steady which wouldn’t be possible in case the private sector couldn’t access credit.

Is a high fiscal stimulus sustainable – global comparison?

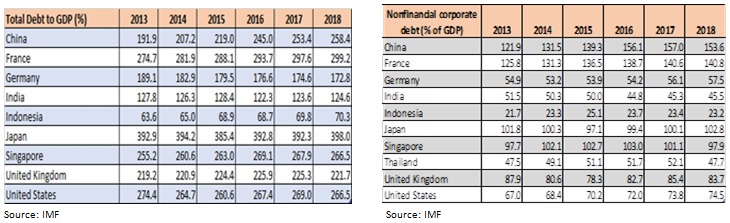

As can be seen from the table below, despite a rise in household & Govt leverage over the past few years, India has maintained a very healthy & stable “Country debt” (Govt+ household+ Corporate) to GDP profile due to deleveraging of the private sector. While India so far has been understandably restrained, maybe it’s time for India to announce a meaningful fiscal stimulus to correct the demand side growth challenges (household+ corporate + banking) rather than the stop-gap measures like reducing taxes moderately which don’t work in a low confidence channel. In fact, India’s external profile & debt sustainability is more reliant on achieving our potential growth sustainably than a cosmetic reduction in our fiscal metrics.

The way ahead

The literature on historical economic recoveries shows that policy response matters and that slow recoveries are typically caused by the urgent need for balance sheet repair after financial crises. The abruptness and the depth of the current shock, including the devastating effects on labour market, are also unprecedented which necessitates urgent & strong policy action.

An important dimension, we have been expecting is a sizeable bond buying program from RBI to support the expanded fiscal. The format globally now is evolving around monetary expansion supporting fiscal policy and India needs to do the same to ensure minimum disruption to the bond market & enable strong transmission of policy rate cuts. Given the risk averseness in the banking system on mark to market risks, there is currently a very low appetite for duration even at the current borrowing numbers. If Govt. announces a policy stimulus without corresponding monetary support, it could result in significant hardening of yields & threaten macro-stability. Its critical to bring the risk free (sovereign) bond yield down as it acts as a bellwether for other borrowers in the economy who cannot be incentivized to invest if their expected revenues (nominal GDP growth) is even lower than their borrowing cost (risk free rate +premium). The FY21 nominal GDP growth rate is expected to be substantially lower than the prevailing bond yields making any fiscal expansion self-defeating. Hence, the financing of the expanded borrowing program either through Open Market Operations or direct placement with RBI has to be put in place before India embarks on fiscal expansion. Given the massive liquidity & general risk aversion amongst banks, a simple solution for RBI would also be to hike Held to Maturity (HTM) on incremental Statutory Liquidity Ratio (SLR) purchases for some time to create a natural demand for Government bonds which can be scaled down as credit growth picks up.

However, it is critical that the quality of fiscal spending is towards productive & job creating assets rather than just temporary consumption boost which can create faster aggregate demand in the near term but has lower multiplier, can lead to misallocation of capital & higher future inflation as we witnessed post 2008.

In fact, this is an historic opportunity for India to use this window to correct its macro imbalances. India can use this stimulus to invest in its agri-value chains or to incentivize shifting of manufacturing supply chains locally to create high quality jobs, income growth & establish a stronger foundation for a sustainable growth.

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the stocks may or may not continue to form part of the scheme’s portfolio in future. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.